PRESS RELEASE: Weekly Update – Global Fertiliser Markets – w/e 05.06.2026

UREA – India Tender to Determine Urea Market Direction

PHOSPHATES – Record Sulphur Prices Drive Further Tightness

POTASH – A Stable Market with Modest Upside

AMMONIA – Supply Recovery May Ease Recent Pressures

Global fertiliser markets remain heavily influenced by supply disruptions, geopolitical uncertainty and affordability concerns, with markedly different fundamentals emerging across the major nutrient groups.

The global urea market remains focused on India’s upcoming 1.7 million tonne import tender closing today (8 June), which is expected to provide the next major pricing signal for international nitrogen markets.

Meanwhile, phosphate markets continue to strengthen as record sulphur prices, constrained Chinese exports and ongoing logistical disruptions tighten global supply.

Potash markets remain comparatively stable, while ammonia markets are showing early signs that recent supply tightness may begin to ease.

“Fertiliser markets continue to be driven by geopolitics, trade policy and supply security concerns rather than traditional supply and demand fundamentals,” said Stein Haugan, CEO of Australian Fertilizer Corporation.

UREA

Indicative Range: USD 535 – 670/t CFR

Global urea markets have adopted an increasingly bearish tone ahead of India’s latest tender.

Demand remains subdued across most major importing regions, with many buyers delaying purchases while awaiting greater clarity on market direction. Brazilian imports remain well below last year’s levels, while Southeast Asian producers continue reporting available export tonnes but limited buying interest.

In China, authorities have extended the shipment period for the first tranche of export volumes through September, and floor prices have been removed since they were unworkable in a falling market.

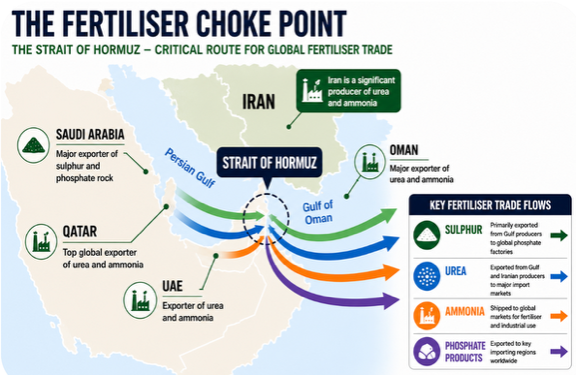

Middle Eastern producers are also struggling to secure sales at desired price levels, while recovering Iranian production continues to add to global availability.

The market now awaits India’s tender outcome, with sentiment suggesting further downside risk unless buying volumes significantly exceed expectations.

PHOSPHATES

Indicative Range:

DAP: USD 930 – 980/t CFR

MAP: USD 900 – 950/t CFR

Phosphate markets remain the strongest of the major nutrient groups.

DAP prices have remained near USD 930-935/t CFR into India, while Brazilian MAP values continue to hold around USD 900/t CFR despite widespread affordability concerns.

The primary driver remains the continued absence of meaningful Chinese phosphate exports combined with a severe escalation in sulphur costs. Sulphur prices have now exceeded USD 800/t FOB, placing substantial cost pressure on phosphate producers globally.

Additional supply challenges are emerging from disruptions to Middle Eastern trade routes and production cutbacks by several major producers.

Unless Chinese exports resume, sulphur prices decline materially, or logistical conditions improve, phosphate markets are expected to remain structurally tight for the foreseeable future.

POTASH

Indicative Range: USD 400 – 450/t CFR

Potash markets remained broadly stable this week.

Brazilian MOP prices have shown little movement despite remaining approximately 10% above levels seen at the beginning of the year. While demand remains somewhat cautious, supply availability is also limited, with many suppliers effectively sold out through August.

Recent Indonesian tender activity has provided additional support to regional pricing, although broader macroeconomic pressures continue to weigh on farmer purchasing decisions.

Potash continues to offer the strongest affordability proposition among the major nutrient groups and remains well supported by underlying agricultural demand.

AMMONIA

Indicative Range: USD 750 – 950/t CFR

Global ammonia markets remain elevated but are beginning to show signs of potential softening.

Several major Southeast Asian facilities are returning to operation, including production assets in Malaysia, Australia and Indonesia. These restarts represent the first meaningful improvement in the supply outlook since disruptions intensified earlier this year.

The easing of supply constraints has already begun influencing market sentiment, with Tampa ammonia settlements moving lower this week.

While prices remain historically strong, the balance of risks is gradually shifting from further increases towards a period of stabilisation or modest correction.

OUTLOOK

Global fertiliser markets remain dominated by five key themes:

• India’s 1.7 million tonne urea tender

• Chinese fertiliser export policy uncertainty

• Record sulphur prices above USD 800/t FOB

• Ongoing Strait of Hormuz-related supply disruptions

• Recovery of ammonia production across Southeast Asia

Urea markets remain vulnerable to further weakness, phosphate markets remain fundamentally bullish, potash continues to demonstrate stability, while ammonia may be approaching a period of modest correction as additional supply returns to the market.

“In a complex geopolitical landscape, fertilisers are no longer simply agricultural inputs; they have evolved into a sovereign commodity as strategically important as energy and food security itself,” said Mr. Stein Haugan, CEO of Australian Fertilizer Corporation.

ENDS