PRESS RELEASE: Weekly Update – Global Fertiliser Markets – w/e 01.05.2026: Affordability pressures and geopolitical disruption begin to fragment global nutrient markets

Global fertiliser markets showed early signs of divergence this week, as affordability constraints and seasonal demand shifts began to weigh on nitrogen and phosphate activity, while ammonia and potash remained supported by supply-side pressures and logistics.

“What we are seeing now is not a uniform tightening cycle, but a market beginning to split,” said Stein Haugan, CEO of Australian Fertilizer Corporation.

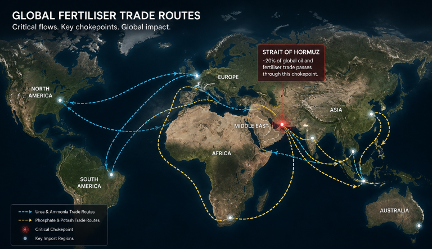

“Affordability is starting to cap demand in urea and phosphates, while supply disruptions — particularly around the Strait of Hormuz — continue to underpin ammonia and freight-linked nutrients.”

Urea

Indicative Range: USD 770 – 900/t CFR

Following a recent Indian tender, the global urea market has entered a period of low activity, with trading interest described as muted across most regions.

Prices are softening under a combination of affordability constraints, seasonal slowdown, and available May cargoes, raising questions as to whether the market is entering a correction phase or simply pausing ahead of further Indian demand.

Producers are actively offering material, but buyer engagement remains limited. Offers of Algerian product at USD 850/t FOB and Nigerian tonnes into Brazil at USD 770/t CFR have failed to attract meaningful uptake.

Middle East supply remains constrained due to the ongoing closure of the Strait of Hormuz, with limited exceptions such as southern Oman. At the same time, Egyptian exports have declined materially, with January shipments down 36% year-on-year.

Structural tightening may emerge longer term, however, as bilateral offtake agreements — including recent Indonesia-linked contracts — continue to reduce spot market availability.

The market remains highly sensitive to India. In the absence of a new tender, prices may come under further pressure as buyers avoid high-cost inventory positions.

Phosphates

Indicative Range:

DAP: USD 865 – 1,000/t CFR

MAP: USD 900 – 1,000/t CFR

Phosphate markets remain fundamentally tight but commercially inactive, as high prices continue to limit buyer participation.

India has issued an unusually large tender for 1.2 million tonnes of DAP and 400,000 tonnes of TSP, highlighting the scale of supply concern. However, market engagement is expected to remain limited until pricing clarity emerges.

Supply constraints persist across key producers. Morocco’s OCP is reportedly reducing Q2 output, while Chinese producers are lowering operating rates amid elevated sulphur costs and ongoing export restrictions.

Brazilian MAP prices have risen sharply over recent weeks but are now encountering demand resistance, with limited transactions reported despite offers approaching USD 1,000/t CFR.

Across the sector, the disconnect between supplier pricing and buyer affordability continues to widen, with government support mechanisms increasingly required to sustain imports in key markets such as India.

Potash

Indicative Range: USD 400 – 420/t CFR

Potash prices held broadly stable this week, supported by firmer freight rates and steady supplier positioning.

Brazil remains the key reference market, with buyers resisting purchases above USD 400/t CFR after recent volume accumulation. Suppliers, however, continue to target higher levels into the mid-year application season.

Freight and logistics costs are re-emerging as a supporting factor, contributing to upward price expectations despite relatively subdued spot demand.

India contract negotiations have resumed, with a narrowing gap between buyer and seller expectations suggesting a near-term resolution.

Ammonia

Indicative Range: USD 800 – 900/t CFR

Ammonia markets remain firm, with tightening supply continuing to support upward pricing pressure.

A series of outages and maintenance events — including the upcoming shutdown of Indonesia’s PAU facility — are removing material from an already constrained market east of Suez.

At the same time, disruption through the Strait of Hormuz continues to limit trade flows, reinforcing supply tightness and increasing delivered costs.

Demand from India remains robust ahead of the Kharif season, though buyers are increasingly resistant to higher price levels, drawing instead on inventories and alternative supply sources.

While Chinese domestic prices have softened slightly, this has yet to materially impact international availability.

Outlook

The global fertiliser market is entering a more complex phase, characterised by divergence between nutrients.

Nitrogen and phosphates are increasingly constrained by affordability, while ammonia and potash remain supported by supply disruption, freight costs, and geopolitical risk.

Key variables to monitor:

• Strait of Hormuz disruption

• India tender activity

• China export policy

• Farmer affordability and demand response

“In simple terms, supply is no longer the only story,” Mr Haugan said.

“Demand — and the ability to pay — is now becoming the critical balancing force across global fertiliser markets.”

ENDS